Client behaviour advisory firm Circana unveiled its newest meals trade insights, detailing altering shopper spending patterns and gross sales of fast-moving shopper items (FMCG).

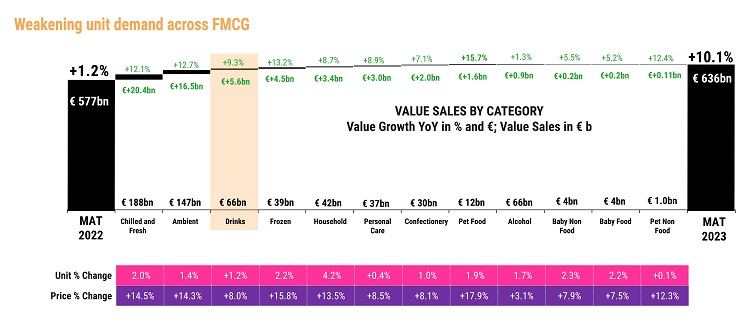

In its newest FMCG Demand Indicators report, Circana information reveals that FMCG worth gross sales proceed to be pushed virtually fully by inflation, which has grown by an extra 10.1% year-on-year (YoY) to achieve €636 billion. There may be weakening unit demand throughout FMCG that’s not anticipated to get better earlier than the second half of 2024 as European shoppers proceed to purchase much less, with a 1.3% decline in unit gross sales over the previous 12 months.

“Inflation-fatigued shoppers are favouring discounted and deal-driven purchasing,” Ananda Roy, World SVP, Strategic Development Insights, Circana, instructed FoodNavigator. “Regardless of these challenges, prospects for progress and resilience lie in innovation, sustainability, and strategic pricing methods to face up to future shocks,” Roy added.

Immediately’s meals trade is dealing with “a brand new period in pricing”, Roy stated. On this period of shifting shopper loyalties, producers and retailers should reevaluate their pricing methods to boost demand, safeguard quantity, and obtain unit progress. Meals and beverage manufacturers have to undertake a recent strategy to pricing, avoiding adjustments that erode margins with out producing appreciable quantity will increase. “The looming risk of a value struggle underscores the significance for manufacturers to keep away from a race to the underside,” Roy detailed.

Evolving shopper buying habits

The report revealed that at this stage within the cost-of-living disaster, buyers have adopted a spread of behaviours to average the impression of rising costs. Procuring round, shopping for smaller packs of meals, shopping for extra from discounters and being good about offers are standard methods at the moment’s shoppers are purchasing.

Shoppers are additionally extremely price-focused when attempting merchandise. Subsequently, if a product isn’t on sale or accessible at a lovely value, they’ll purchase one other model, change to a private-label choice or transfer to a unique retailer altogether.

There may be additionally proof that classes, merchandise, and even out-of-home consumption as soon as thought of ‘on a regular basis’ at the moment are seen as discretionary by buyers. “This doesn’t imply they’re not purchased in any respect,” Roy stated. As an alternative, extra typically, a product turning into discretionary suggests shoppers are shopping for much less of it, making what they’ve of their cabinets last more or deferring their buy.

“All of those coping behaviours—shopping for extra from discounters, switching to personal label manufacturers and shopping for solely important objects—will solely go up to now, although,” Roy stated. Continued unit decline not solely sees shoppers purchasing otherwise, however in addition they should make troublesome selections about what they’ll and may’t afford each time they store. “Generally, the one inexpensive choice open to them is to eat much less, significantly since inflation continues to be targeted on on a regular basis meals objects,” Roy added.

Difficult shopper developments set to proceed

Projections point out that the pressures shoppers face in making buying selections will proceed for the foreseeable future. “As world turmoil and uncertainty proceed, most of the difficult shopper developments and behaviours we’ve seen over the past two years are set to proceed for an additional 12 months,” Roy shared.

Inflation has eased significantly in latest months. Nevertheless, this could sometimes be anticipated to result in a restoration in demand. “That unit gross sales have continued to drop exhibits how financially distressed shoppers are and the way essentially the cost-of-living disaster has modified their purchasing habits,” added Roy.

A number of elements clarify why demand has remained unexpectedly weak, the report discovered. Whereas enterprise confidence and shopper sentiment have improved previously six months, companies inflation has begun. “Sky-high insurance coverage prices, rents and mortgage rates of interest are squeezing incomes in nominal phrases,” Roy shared.

Latest information about meals costs easing additionally must be put into context, Roy stated. Whereas FMCG value inflation is reducing, costs stay a lot increased than in January 2021. As flagged in Circana’s earlier Demand Indicators report, ‘disinflation’ drives class pricing quite than deflation. “The online impact is that European buyers proceed to really feel a lot worse off than they did two years in the past,” Roy stated.

Dropping market share and gaining it again once more

Meals and beverage manufacturers are lacking market earnings as a result of personal labels proceed gaining floor, the report states, which follows the rise of grocery store personal label manufacturers and fewer new product launches. Circana’s final Demand Indicators report 2023 flagged a ‘tipping level’ for personal labels and indicated that European shoppers more and more understand it as the standard selection. Six months on, the march of personal labels continues. “What’s extra, personal labels have gotten more and more premium,” added Roy.

Now accounting for 39% of grocery gross sales within the European Union (EU), the personal label phase is value €246 billion to retailers, having grown its worth share by an extra 2.2 share factors within the final 12 months, to June 2023. Two years in the past, that share stood at 35%.

Nevertheless, private-label growth isn’t anticipated to proceed. “It’s essential to notice that there will likely be a restrict to personal label progress,” Roy shared. In at the moment’s European retail atmosphere, retailers, like manufacturers, are the largest drivers of worth, innovation and footfall. Retailers need personal labels to compete vigorously with manufacturers however don’t need manufacturers to fail.

“Personal labels have to be considered critical competitors, and types should determine sources of progress and alternative, significantly within the areas of innovation, sustainability and pricing, and enhance their resilience to future shocks,” stated Roy.

Now’s a tricky atmosphere to take action, nonetheless. “Creating new demand is way from simple proper now, however our evaluation exhibits it may be accomplished,” Roy shared. Intuitive, well-targeted innovation sits on the coronary heart of a model success story and pushing arduous on new product growth (NPD) offers buyers recent causes to attach with a meals and beverage class.

Trying forward, the main focus, the report asserts, is on inspiring buyers and positioning merchandise as versatile substances that can be utilized to create thrilling meals.

“Over the subsequent 12 months, the profitable manufacturers will put money into daring, agenda-setting NPD that responds to new shopper behaviours and consumption moments, not those that tinker across the edges of their portfolios,” Roy added.